Issue No. 7 — Consumer Steadies While Server Ecc Splits

- Samsung's reported push for up to 20% 3Q26 DRAM contract price increases, corroborated by TrendForce's 13–18% QoQ forecast, reflects AI-server-driven new-channel tightness that has not yet translated into equivalent secondary market firming — the aftermarket continues to price on available supply, not forward contract expectations.

- Low-density DDR4 and DDR3 segments are showing the most constructive spot dynamics in new-channel data per TrendForce's weekly update, a directional alignment with DDR4 32GB's Healthy DDI 67 reading and DDR3 ECC 16GB's stabilization in The DRAM Resource Pricing Survey this cycle.

- Lenovo's publicly stated view — that elevated memory pricing represents a structural 'new normal' persisting into 2030 — reinforces a longer-dated constructive thesis for ITAD operators, but near-term secondary availability remains adequate across most consumer segments, capping upside in Stage 2 and Stage 3 bands.

- AI-driven server refresh compression continues to load ITAD decommissioning pipelines with inbound DDR4 ECC inventory; elevated inbound volumes at compressed institutional buy interest are the operative dynamic behind DDR4 ECC 32GB's distressed DDI reading this cycle.

- SK hynix's advancing Nasdaq ADR listing targeting ~$30B for HBM and fab expansion underscores structural capital commitment to high-bandwidth memory at the expense of commodity DRAM capacity growth — a supply-side dynamic that supports longer-dated secondary server memory valuations even as near-term pricing softens.

↑ FIRMING — DDR4 ECC 64GB & DDR4 32GB

DDR4 ECC 64GB posts the cycle's clearest constructive signal, with both Stage 2 and Stage 3 values moving directionally higher and the DDI advancing to 50 — consistent with opportunistic institutional re-engagement at legacy high-density server price levels that have compressed sufficiently to attract renewed buy-side interest. DDR4 32GB holds Healthy at DDI 67, the strongest score on the board this cycle, with Stage 2 and Stage 3 bands steady and adequate buy-side depth maintained — mid-density consumer DDR4 remains the most defensible disposition posture in the current environment.

↓ DISTRESSED & SOFTENING — DDR4 ECC 32GB & Consumer DDR5

DDR4 ECC 32GB is the cycle's most significant deterioration story, collapsing to Distressed at DDI 37 — a 25-point decline from Issue 6's 62 — as elevated inbound decommissioning volumes collide with subdued institutional buy interest for legacy mid-density server ECC, creating the weakest disposition environment on the current board. Consumer DDR5 tiers compound the softness: DDR5 16GB retreats further in both Stage 2 and Stage 3 bands, and DDR5 32GB stabilizes at a Cautionary DDI 57 but remains well off its Issue 5 peak, reflecting secondary channel normalization as enterprise DDR5 transition volumes continue to mature into resale supply.

Stage 2 and Stage 3 values from The DRAM Resource Pricing Survey, 30-day lookback. Directional arrows reflect week-over-week movement. Stage 1 (Used Wholesale) is subscriber-only.

| DRAM Segment | Stage 1 — Used Wholesale | Stage 2 — Private Aftermarket | Stage 3 — Public Used |

|---|---|---|---|

| DDR4 8GB | 🔒 Subscribers Only | $25–$31 ↓ | $31–$38 ↓ |

| DDR4 16GB | 🔒 Subscribers Only | $50–$70 → | $64–$78 → |

| DDR4 32GB | 🔒 Subscribers Only | $110–$200 → | $150–$185 → |

| DDR5 16GB | 🔒 Subscribers Only | $120–$160 ↓ | $150–$185 ↓ |

| DDR5 32GB | 🔒 Subscribers Only | $220–$285 → | $290–$350 → |

| DDR4 ECC 32GB | 🔒 Subscribers Only | $95–$155 → | $125–$150 → |

| DDR4 ECC 64GB | 🔒 Subscribers Only | $200–$275 ↑ | $245–$300 ↑ |

| DDR5 ECC 64GB | 🔒 Subscribers Only | $1,000–$1,450 | $1,410–$1,715 |

| DDR3 ECC 16GB | 🔒 Subscribers Only | $18–$50 → | $27.5–$34 → |

DDI scores updated from Issue 6. Scores in parentheses reflect week-over-week change.

DDI Highlights: DDR4 ECC 32GB's plunge to Distressed at DDI 37 (−25 vs. Issue 6's 62) is the defining — and most actionable — move of this cycle, as Stage 2 and Stage 3 values hold steady directionally but institutional buy conviction has materially eroded, leaving operators with legacy mid-density server ECC lots in an increasingly difficult liquidation environment. DDR4 8GB edges higher to Cautionary at DDI 53 (+6 vs. Issue 6's 47), with both Stage 2 and Stage 3 bands softening directionally — the DDI improvement reflects a base-effect recovery from an oversold prior reading rather than genuine demand acceleration. DDR3 ECC 16GB advances to DDI 56 (+10 vs. Issue 6's 46), with flat Stage 2 and Stage 3 bands suggesting stabilization rather than recovery, consistent with TrendForce's observation of constructive dynamics in low-density legacy segments. DDR4 32GB holds Healthy at DDI 67 (+7 vs. Issue 6's 60), the board's top score, with both pricing bands flat and secondary availability characterized by depth sufficient to support institutional volume without meaningful price concession.

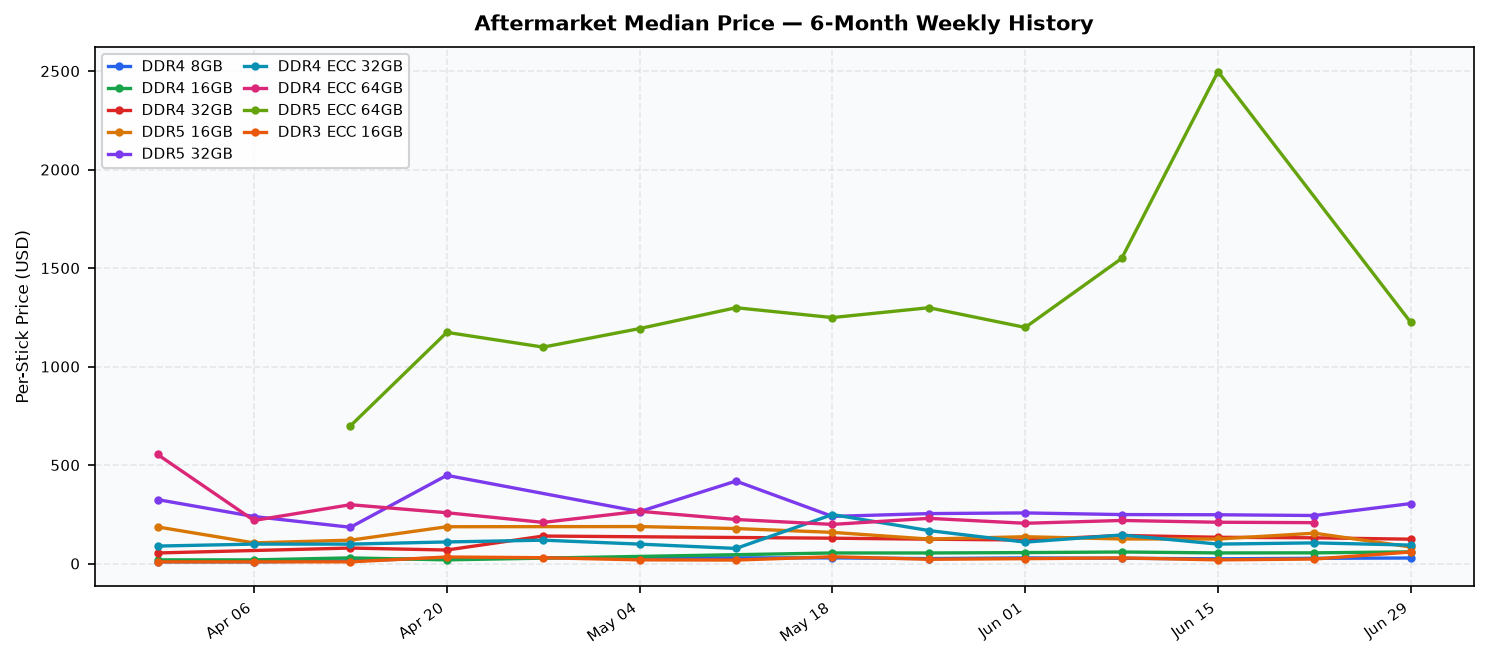

Weekly median (p50) per-stick price from The DRAM Resource Pricing Survey, aftermarket used. Stage 1 wholesale excluded. March 30 – June 22, 2026.

ITAD Disposition Timing — Issue 7 Signal

Disposition posture diverges sharply by segment this cycle — operators should treat the DDI board as a tiering tool rather than a single directional guide.

- Server ECC — Accelerate liquidation of DDR4 ECC 32GB lots where holding costs are material; DDI 37 (Distressed) and the absence of directional price recovery signal limited near-term upside, while DDR4 ECC 64GB's directional firming justifies a neutral-to-hold posture for high-density server lots pending further Stage 2 confirmation.

- Consumer DDR4 — Maintain neutral posture on DDR4 32GB (DDI 67, Healthy) where pricing depth supports orderly disposition without urgency; DDR4 16GB's flat bands and Cautionary DDI 57 warrant selective liquidation pacing rather than bulk clearing.

- Consumer DDR5 — Hold DDR5 32GB (DDI 57, Cautionary) through the next cycle pending signal on whether the flat Stage 2 and Stage 3 bands represent stabilization or a prelude to further softening; accelerate DDR5 16GB disposition where inventory carrying risk is elevated, given continued directional price weakness in both published bands.