Issue No. 6 — Broad Cautionary Rotation Across The Board

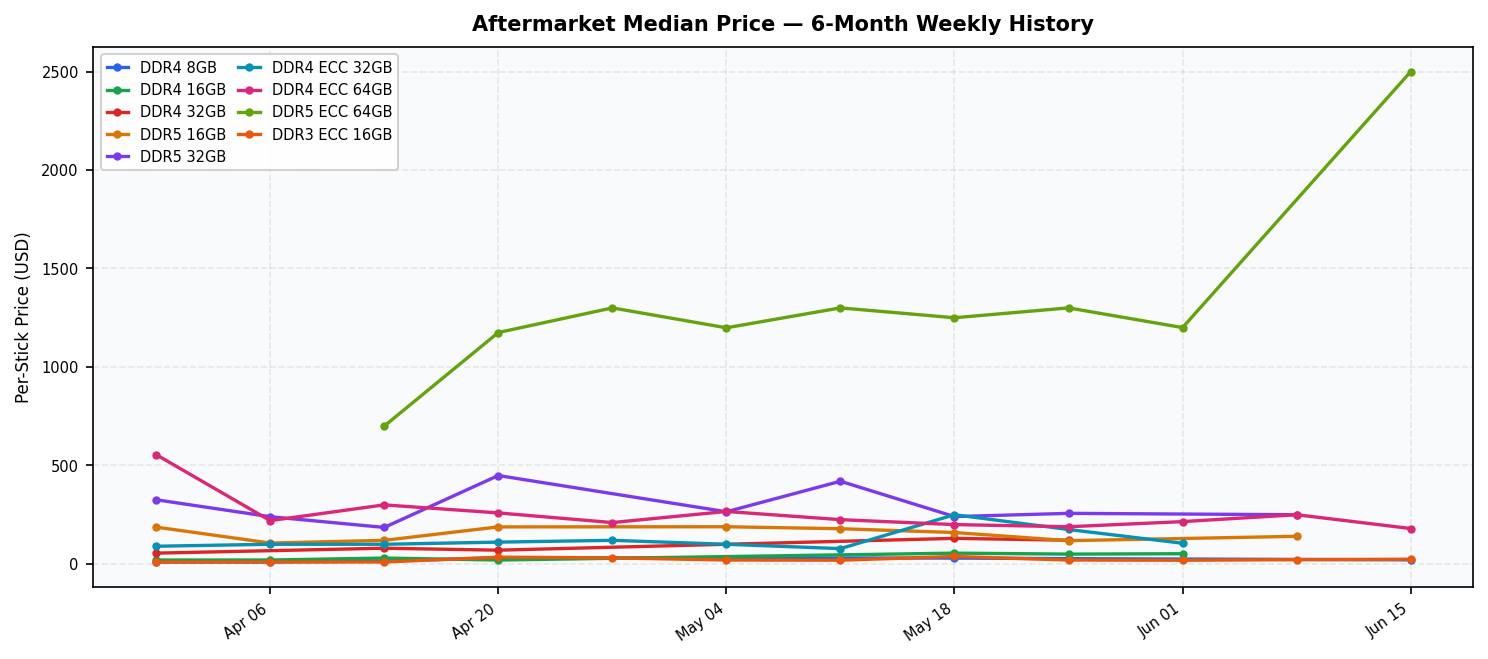

- DDR5 ECC 64GB Stage 2 and Stage 3 values have moved directionally lower this cycle, marking a meaningful reversal from the recovery trajectory sustained through Issues 4 and 5 — the segment now sits in Cautionary territory for the first time this publication cycle.

- DDR4 ECC 64GB is the lone segment posting a positive directional signal this issue, with both Stage 2 and Stage 3 values firming modestly — a development that may reflect opportunistic buy-side absorption of legacy server lots at compressed price levels rather than a structural demand recovery.

- Consumer DDR5 32GB has retreated from its Issue 5 peak of DDI 84 (Strong) into Cautionary territory, with Stage 2 bands narrowing downward as enterprise DDR5 platform absorption shows early signs of saturation in secondary channels.

- E-Scrap News reports that the US data center construction boom and AI-driven refresh cycle compression — now approaching 18-month intervals at some hyperscaler operators — are structurally loading the ITAD decommissioning pipeline, a dynamic that could translate into elevated inbound server memory volumes and additional supply-side pressure on server ECC pricing in coming cycles.

- Aletheia Capital's projection of a ~30% rise in server DRAM ASPs in Q3 2026 remains a constructive longer-dated signal for ITAD operators, but current aftermarket data from The DRAM Resource Pricing Survey does not yet reflect that trajectory — disposition timing relative to new-channel price inflection is the operative variable for operators managing hold-versus-liquidate decisions this cycle.

↑ RESILIENT — DDR4 ECC 32GB & DDR4 ECC 64GB

DDR4 ECC 32GB holds Healthy at DDI 62 — the only segment above the Healthy threshold this cycle — with Stage 2 values maintaining depth and buy-side conviction intact for mid-density legacy server lots that remain viable in cost-sensitive refresh environments. DDR4 ECC 64GB, despite its Cautionary DDI reading of 48, posts the cycle's only positive directional price signal across both Stage 2 and Stage 3 bands, suggesting that selective institutional demand is beginning to re-engage with legacy 64GB server lots at current price levels. Taken together, these two server ECC segments represent a tentative floor-finding dynamic within an otherwise broadly softening cycle.

↓ SOFTENING — DDR5 ECC 64GB, DDR5 32GB & Consumer Tiers

DDR5 ECC 64GB's Stage 2 and Stage 3 values have moved directionally lower this cycle, pulling the segment's DDI to 58 (Cautionary) and unwinding the constructive momentum that had defined it through Issues 4 and 5 — operators carrying high-density server DDR5 lots should reassess hold timelines against the risk of further near-term compression. Across consumer tiers, DDR5 32GB has reversed sharply from its Issue 5 Strong reading, DDR5 16GB continues its extended Cautionary streak, and DDR4 32GB has softened further — a convergence that points to loosening secondary availability as enterprise DDR5 transition volumes begin to normalize into the resale channel.

Stage 2 and Stage 3 values from The DRAM Resource Pricing Survey, 30-day lookback. Directional arrows reflect week-over-week movement. Stage 1 (Used Wholesale) is subscriber-only.

| DRAM Segment | Stage 1 — Used Wholesale | Stage 2 — Private Aftermarket | Stage 3 — Public Used |

|---|---|---|---|

| DDR4 8GB | 🔒 Subscribers Only | $25–$33 ↑ | $32–$39 ↑ |

| DDR4 16GB | 🔒 Subscribers Only | $45–$58 | $60–$73 |

| DDR4 32GB | 🔒 Subscribers Only | $110–$130 | $145–$175 |

| DDR5 16GB | 🔒 Subscribers Only | $115–$145 | $145–$180 |

| DDR5 32GB | 🔒 Subscribers Only | $225–$265 | $290–$355 |

| DDR4 ECC 32GB | 🔒 Subscribers Only | $175–$270 | $225–$275 |

| DDR4 ECC 64GB | 🔒 Subscribers Only | $190–$255 ↑ | $270–$330 ↑ |

| DDR5 ECC 64GB | 🔒 Subscribers Only | $1,300–$1,410 ↓ | $1,550–$1,890 ↓ |

| DDR3 ECC 16GB | 🔒 Subscribers Only | $20–$36 ↑ | $28.5–$35 ↑ |

DDI scores updated from Issue 5. Scores in parentheses reflect week-over-week change.

DDI Highlights: DDR5 32GB suffers the sharpest single-cycle decline on the board, falling to Cautionary at DDI 56 (−28 vs. Issue 5's 84), as Stage 2 and Stage 3 values compress and the supply tightness that drove its prior Strong reading shows early signs of relief — this reversal is the defining move of Issue No. 6. DDR4 32GB retreats to Cautionary at DDI 60 (−22 vs. Issue 5's 82), extending the consumer DDR4 softening trend and reflecting broadly adequate secondary availability against subdued institutional buy interest. DDR4 ECC 64GB edges higher to DDI 48 (+8 vs. Issue 5's 40), the cycle's sole positive DDI delta, with directional price firming in both Stage 2 and Stage 3 bands indicating nascent buy-side re-engagement at legacy server ECC price levels. DDR4 16GB is unrated this cycle, carrying no DDI score; this segment was previously tracked at DDI 69 in Issue 5 and has been removed from the DDI board this issue pending signal stabilization.

Weekly median (p50) per-stick price from The DRAM Resource Pricing Survey, aftermarket used. Stage 1 wholesale excluded. March 30 – June 22, 2026.

ITAD Disposition Timing — Issue 6 Signal

With seven of nine rated segments in Cautionary territory and DDI momentum broadly negative, Issue No. 6 calls for a defensive disposition posture across most categories — the exception is legacy DDR4 server ECC, where early price firming merits a reassessment of accelerated liquidation strategies.

- Server ECC (DDR4 ECC 32GB / DDR4 ECC 64GB): Neutral-to-hold on DDR4 ECC 32GB, which retains Healthy status and the deepest DDI on the server side; consider selectively accelerating DDR4 ECC 64GB lots where the positive directional price signal aligns with near-term processing capacity, as the firming may prove transient given broader market softness.

- Consumer DDR4 (DDR4 8GB / DDR4 32GB): Neutral — Stage 2 and Stage 3 values are compressing or flat across consumer DDR4 tiers, and the absence of buy-side catalyst argues against forced liquidation; operators with storage flexibility should hold for improved signal clarity in the next cycle.

- Consumer DDR5 (DDR5 16GB / DDR5 32GB): Neutral-to-accelerate for bulk DDR5 32GB positions given the severity of the DDI reversal (−28 this cycle); continued carry cost on large DDR5 32GB lots is increasingly difficult to justify against a backdrop of normalizing secondary availability and the absence of near-term demand recovery signals in The DRAM Resource Pricing Survey data.